Sustainable Transport Infrastructure Charging and Internalisation of Transport Externalities

The objective of the study was to assess the extent to which the “user pays” and the “polluter pays” principles were implemented. This allowed the European Commission to take stock of the progress of Member States towards the goal of full internalisation of external and infrastructure costs of transport and to identify options for further internalisation.

The scope of the study involved all external costs, all transport modes and, geographically, EU28 plus Norway, Switzerland, USA (2 States), Canada (2 provinces) and Japan.

To realise the general objective and address the scope of the study information has been collected extensively about: infrastructure costs (i.e., investment, renewal and operating), transport-related charges, earmarking of fiscal revenues and compensations paid by the users.

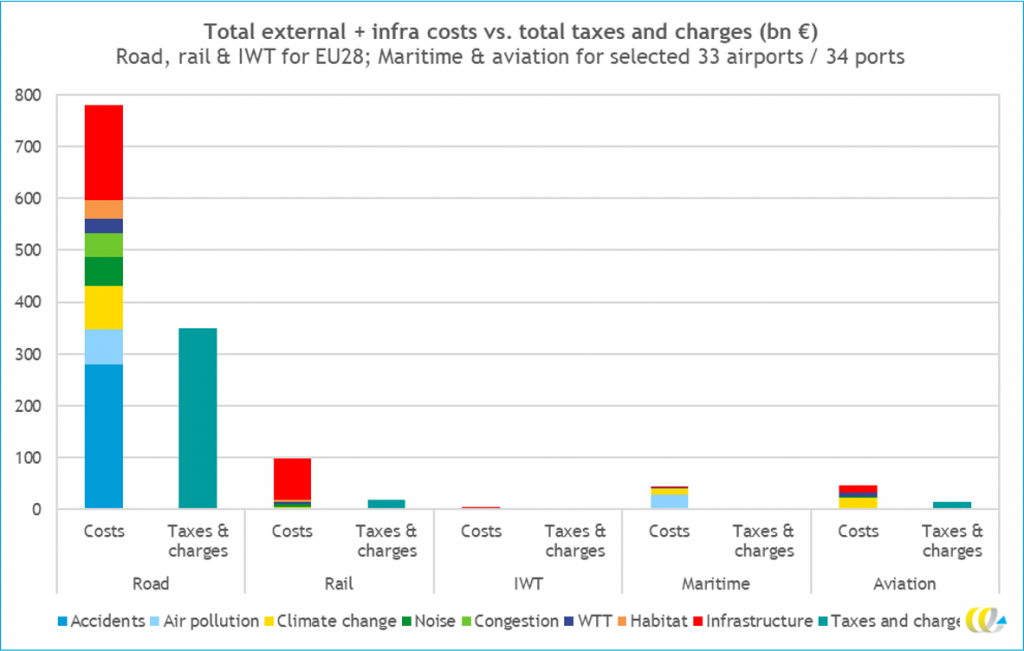

The analyses carried out in this study showed that the transport taxes and charges levied in the EU Member States are in general insufficient to fully internalise the external and infrastructure costs of transport.

For most vehicle categories, only 15% to 25% of the external and infrastructure costs are covered by tax/charge revenues. The cost coverage ratio for passenger cars was found higher (about 50%), which was mainly because of the relatively high fuel and vehicle tax levels applied in (some of) the EU Member States for these vehicles. For inland waterways and maritime transport, much lower cost coverage ratios were found (i.e., 6% and 4%, respectively), reflecting the limited tax/charge burden levied on these modes in the EU.

Even if one excludes fixed infrastructure costs from the analyses, the taxes and charges did not cover the external and variable infrastructure costs for most vehicle categories. High-speed trains are an exception, as for these trains the current taxes and charges did cover all external and variable infrastructure costs.

This finding has been supported by the results of the analyses of the marginal social cost (MSC) coverage ratios. Despite the limitations of this analyses, it provides a first indication that there was a lack of charging in accordance with the MSC principle in the EU28.

The revenues from transport taxes and charges in the EU28 were partly earmarked for expenditure for transport infrastructure. However, significant differences did exist between modes. For road transport, about 10% of the taxes/charges are earmarked, while for rail transport this is about 85%. For the other modes, only fragmented data on earmarking was identified, showing that (at least part of) the (air)port charges are earmarked to cover infrastructure expenditures.

Although taxes and charges are efficient policy instruments to reduce the external costs of transport, the study recognize that other types of policy instruments and non-pricing policies (e.g., command-and-control measures and subsidies) may effectively complement tax and charge schemes, for example by providing EU-wide harmonised incentives to invest in certain reduction technologies.

With regard to the activities of the study, TRT was responsible to (i) develop estimations of the external costs related to congestion for all transport modes (quantitatively for road), (ii) elaborate estimations of the infrastructure costs for rail mode and with respect to all categories of external costs and (iii) support data collection, as country expert of Italy.

For more information

- Publication – Sustainable Transport Infrastructure Charging and Internalisation of Transport Externalities

- Executive summary

- Update of the Handbook on external costs, which includes an analysis of the total and average external costs: Handbook

- More information available on the webpage.